{{THIS SPECIAL REPORT ON ELECTRIFICATION AND MARKET DESIGN WAS RESEARCHED WITH THE SUPPORT OF THE DANISH WIND INDUSTRY ASSOCIATION.

A}} seemingly unsolvable challenge of opening up wholesale electricity markets to renewable energy is spot prices driven so low that investment signals get stuck on permanent red. Renewables are harder hit financially than fossil fuel. Finding a fix for the market design failure is exercising the wits of many in industry and government. Their efforts may be converging on a solution.

The irony is inescapable. Renewable energy, labelled for years as too expensive, is in danger of becoming a victim of its own success. In reducing electricity prices for everybody it is busy cannibalising its own market revenues. The more the wind blows, the sun shines and demand is saturated, the greater the decline in prices on wholesale markets. Cheap electricity benefits consumers, but it becomes a problem when producers fail to make enough money to cover their costs, let alone enough profit to invest in the next power plant required.

The particular problem for renewable energy is that while other generators can sell their output when prices are high, it cannot. More expensive generation moves in to the market and pushes up prices during wind lulls and sunless hours when renewable energy producers are unable to respond to rising demand. During these high price periods, the more competitive bidders among non-renewable generators can make up for losses endured when prices are low. For renewables that is not an option.

In Denmark, where wind energy supplies around 40% of electricity, wind turbine owners are feeling the pinch. Over the course of 2016, the average price paid for wind energy was 10% below the general market price, which was already pushed low by the high volume of wind on the market, says Christian Kjaer, CEO of the Danish Wind Turbine Owners association.

Kjaer’s observation of what happens in practice is borne out in theory. In a recent report on energy pricing, the European Commission acknowledges that wind power decreases wholesale prices. “Econometric analysis suggests that every percentage point increase in renewable share reduces the wholesale electricity price by €0.4/MWh in the EU on average; the actual reduction depends on the regional market and the fuel source being replaced by renewables. The impact of renewables is greater (€0.6 - 0.8/MWh) in north-western Europe, the Baltics and central and eastern Europe.”

ZERO MARGINAL COST

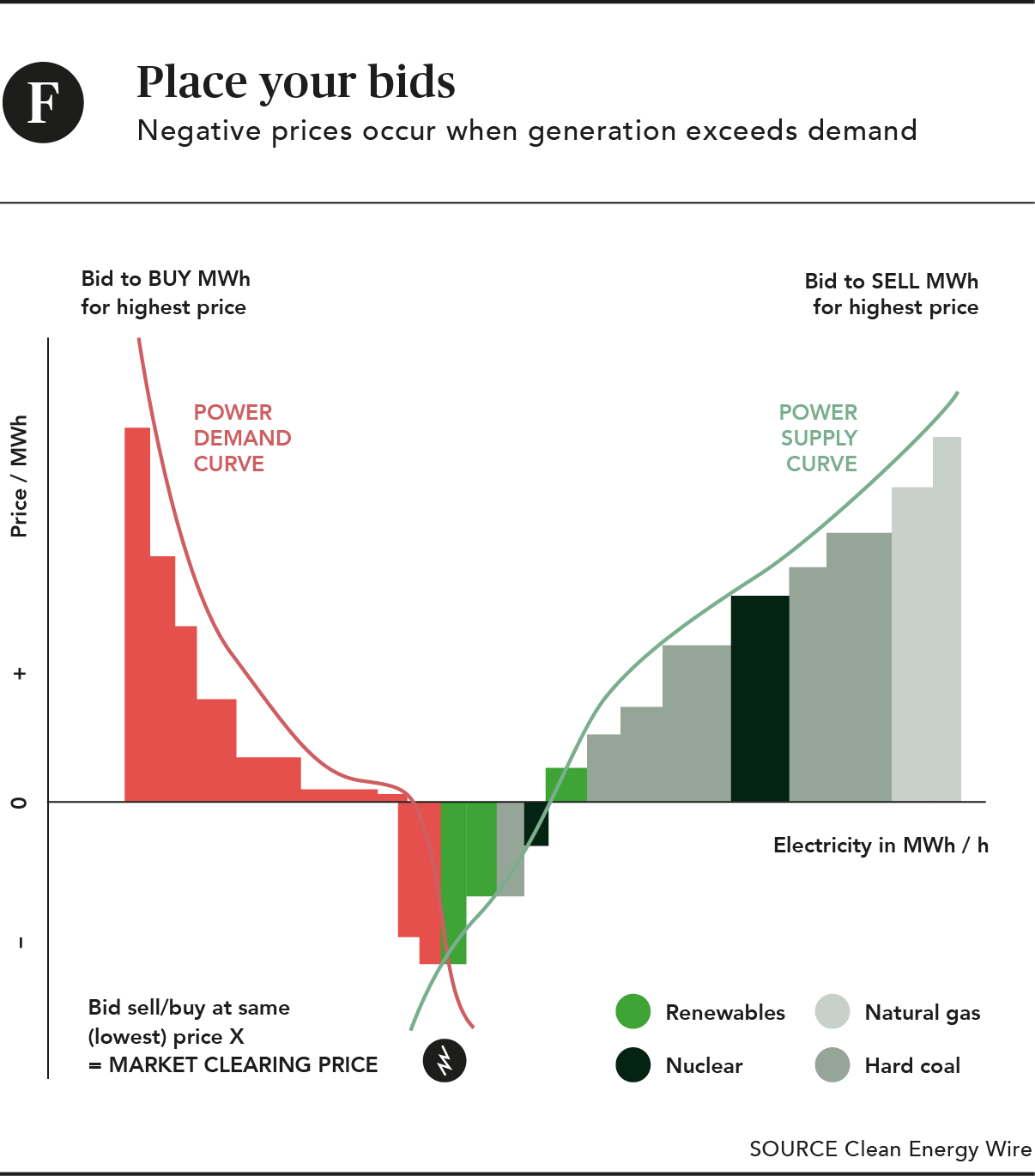

The problem lies in the market design. Across Europe, North America, Australia and elsewhere electricity prices are decided in short-term “energy-only” wholesale markets. Bi-lateral trades are also a part of the global electricity business as are long term power purchase contracts between seller and buyer, but wholesale markets tend to set the reference price outside of auctions for new capacity. An energy-only market operates on the basis of what it would cost to produce the next unit of electricity generated here and now, referred to as the marginal cost, which ignores the lifetime capital and running costs of the plant, which a power purchase contract includes.

In a world of fluctuating fuel prices, using marginal cost as the price setter to balance supply and demand serves consumers well. As demand fluctuates during the day, so does the marginal price. It rises when demand outstrips supply to pull in more generation and drops when demand is met, pushing unneeded generation offline.

Renewable energy producers have lower running costs than nuclear, gas and coal. They can consistently undercut their competitors on marginal cost. With no fuel bills to pay, their marginal costs lie around zero and in times of low demand and high production, the market clearing price can be zero or even turn negative, meaning that electricity retailers are paid to take electricity out of the system before it destabilises. For conventional generators, operating through a short period of negative prices can often be cheaper than stopping and restarting equipment, which is why they pile on the price pressure. Renewable energy producers respond with ever lower bids.

A FUNDAMENTAL FLAW

As the German EEX electricity exchange points out, negative prices and the principle of “scarcity pricing” are not generally bad. They work to provide customers with the cheapest power possible at all times. But as the proportion of renewables on wholesale markets rises, a fundamental flaw in the marginal cost model is becoming increasingly apparent. A market of renewable energy suppliers all presenting bids at zero does not provide a price. Without a well functioning price signal the market mechanism that dispatches generation to exactly match supply and demand, crucial for a stable flow of electricity, breaks down.

“The price levels today are set by the conventional generator but if you assume renewables will replace conventional generators there will be a problem with that traditional model,” says Jochen Kreusel, market innovation manager in the power grids division at ABB Power. “We see competition between renewables and no longer between renewable and conventional generation,” he adds.

Analysts at Citigroup, a bank, believe the time has come to say goodbye to power prices fully driven by fuel prices. Renewables will squeeze the market share of conventional power, they say, “Making thermal power, which is a price setter, a marginal contributor to power price formation.”

Where things get difficult for wind and solar is when they are feeding large volumes into a market that has no flexibility to channel excess supply elsewhere, such as into the heating system, or to an industrial customer offered a good deal to shift its high use period to a different time. In outbidding one another to offload their generation, renewables drive prices down to untenable levels for longer periods. Modelling by the International Energy Agency (IEA) of a largely decarbonised European electricity market by 2050 indicates that very low prices could occur for a third of the time with 43% solar PV and wind. “Beyond this point, the number of hours with zero prices increases further,” it states. •

EXPLAINER MARGINAL COST AND SCARCITY PRICING Spot-price trading of electricity at marginal cost has yet to prove itself as a wholesale market design fit for a renewables future In the wholesale electricity markets of today, which largely emerged with their liberalisation across the United States and Europe in the 1990s, revenue received by generators is solely for units of energy produced. Generators bid energy into the short term market at the marginal cost of its production, which for fossil fuel sources includes the cost of buying fuel.The bids are ranked in ascending order of marginal cost, or the cost of generating power here and now, resulting in what is commonly known as the merit order. Fixed costs, like the capital spent on building a facility, are not specifically taken into account in the bid prices.The purchase price all generators subsequently receive is determined by the marginal cost of production of the last generator satisfying power demand for any specific bid period. The demand is established according to bids placed by electricity purchasers, which are also ranked in merit order based on price (see graph page 21).The marginal price of energy moves up and down during the day. When supply is scarce, prices rise and when it is plentiful they fall. In a market mix dominated by thermal power stations, which trace the majority of their costs to fuel purchases, the wholesale market price of electricity follows underlying fuel prices.By dispatching power on the basis of marginal cost, the aim is to minimise the overall cost of electricity production. Before the advent of renewable energy in the market, prices neatly reflected the generation characteristics of the various conventional power sources.

At the low marginal cost end of the scale, nuclear capacity is relatively inflexible, meaning it is unable to adapt to rapid changes in demand by quickly ramping up or down but is valuable as a baseload supplier. At the other end of the scale, so-called peaking plant, such as gas turbines, produce at a higher marginal cost, but can quickly react in response to calls for more or less energy. In between the baseload and peaker extremes are mid-merit generators like coal plants.As renewable energy penetrates these “energy only” markets, its low marginal cost (it has no fuel bills to pay) enables it to consistently underbid fossil fuel energy technologies and nuclear power. That helps push the most expensive generators at any one time out of the production mix, bringing down the average marginal cost of production and average electricity prices.The market model relies on scarcity pricing. When demand surges or supply collapses, occasional price peaks ensure the generator, in the market providing power with the highest marginal cost, is able to recover its fixed cost. Alternatively, a utility with a diversified generation portfolio can potentially make up for losses on generating sources with high marginal costs on its cheaper marginal cost units.For owners with portfolios consisting of wind and solar capacity alone, however, the effect of scarcity pricing is to reduce their revenue. The more the wind drops and the sun sets, the scarcer that electricity becomes, driving up prices to encourage more expensive generation to come online. The wind and solar plant are almost never able to benefit from these higher prices.The effect is seen on both sides of the Atlantic Ocean in very different wholesale market structures. American markets are fragmented and highly dynamic, with thousands of bid prices reflective of the actual cost at any given moment. In contrast, Europe has focused its efforts on “market coupling” to increase the overall flexibility of the market. The more a market is interconnected, the better the ups and downs of demand and supply can balance one another.

MARGINAL COST FAILURE NOT AN ATTENTION GETTER

The threat of marginal cost pricing to investment in renewables is well recognised, but alleviating it is not given the priority that might be expected

While much attention has been paid to the issue of conventional power companies squeezed out of the market by a cheaper competitor, the problem of renewable energy cannibalising its own market revenues is being left to fester at the bottom of the cauldron of challenges. The risk is that as the proportion of renewable energy grows, the business case for investment in more solar and wind gets rapidly weaker.

In a slew of recent and major reports on reworking market design, including from the International Energy Agency (IEA) and European Commission, the cannibalisation issue receives scant attention beyond being acknowledged. Jochen Kreusel, market innovation manager at ABB Power, offers one explanation for the lack of concern about the financial punishment meted out to renewables in some wholesale markets. “I think they are more or less protected since they are still in the subsidised, protected segment of the market. But it will increasingly be a problem for them, too,” he says, comparing the situation of renewables to conventional generators.

The IEA, in modelling its envisaged European market in 2050, reveals that when wholesale prices are zero or lower, market revenues for variable renewables decline rapidly below the average market price, which it says will remain relatively high at $78/MWh.

But with wind generating 31% of electricity by 2050, the model’s calculated market revenue at $40/MWh, 50% below average market price, “still represents two-thirds of the levelised cost of electricity of onshore wind,” argues the IEA. The cost of wind, with capital cost and operating cost levelised over the entire life of the plant, is assumed at $69/MWh in 2050. Solar, generating 11% by 2050, does not suffer as much. Its revenues are modelled at $70/MWh, or 90% of average market price, “close to the level of utility scale solar PV by 2050.”

Although the model “is almost certainly wrong” in its details, admits the IEA, the indications of trouble ahead are clear. “Taking a scenario with very high shares of wind and solar power could lead to lower average electricity prices and even lower market revenues for wind and solar power generators,” it cautions. But the modelling is the closest the agency comes to detailed examination of the zero marginal cost issue as it affects renewables in the entire 246 pages of its Repowering Markets report on market design.

In Denmark, the owners of over half the nearly 4 GW of onshore wind no longer receiving subsidies sell their output through the wholesale market at below average prices. Christian Kjaer, CEO of Denmark’s Wind Turbine Owners Association is nonetheless unconcerned that neither the IEA nor the European Commission treat the growing case of cannibalisation with any sense of urgency in their recent policy papers. Right now, he says, there are more pressing concerns to deal with at European level if renewables are to grow at the rate needed to fulfil the IEA’s 2050 prognosis. Catherine Mitchell, who heads the Energy Policy Group at Exeter University in the UK, agrees. “It hasn’t really become an existential issue yet,” she says. Kjaer believes that long before renewables have chewed out the bottom of their market, the pressure for lowball bids will be relieved by new price signals.

The problem of renewable energy cannibalising its own market revenues**is being left to fester at the bottom of the cauldron of challenges**

The problem of renewable energy cannibalising its own market revenues**is being left to fester at the bottom of the cauldron of challenges**

WAKE UP CALL

Others are not so sure. Energy-only markets and marginal cost pricing have limitations as a market design and do not encourage up-front investment in technologies like renewables with high capital cost, but low running cost, says Graham Weale, professor of energy economics and politics at Ruhr University Bochum in Germany. He says that as a basic concept spot market prices based on marginal cost are not an investment driver.

“The wholesale market is basically a short-term optimising market so it was always a mistake to think it could ever give long term price signals. Only in a very few cases have power plants built in liberalised markets in the past 20 years been able to recover their full costs in the wholesale market,” he says. This was true even before the financial crisis in 2008 and the market entry of renewables, both of which added further challenges. “And now with more solar and wind the situation is worse because the wholesale price is moving steadily downhill.”

That the entire European power industry is facing a deteriorating investment climate is a view supported by wind industry trade body WindEurope. “The risks faced by investments in capital-intensive assets are too high,” it states in a January 2017 policy paper. “Short-term wholesale electricity prices are too low and volatile to provide and predict adequate returns from the spot market revenues only.”

Mitchell says that while other issues are more immediate, zero marginal cost trouble is brewing on the horizon: “The market model is absolutely a problem for renewable generators without subsidies. The wholesale energy market set-up is to pay back conventional generators, so when you move to technologies with completely different characteristics you will need a new market design.”

ABB’s Kreusel agrees. “We face a fundamental change of the cost structure on the supply side and a need for a fundamental change,” he says. Another expert putting the stress on “fundamental change” is Malcolm Keay at the UK’s Oxford Institute for Energy Studies. Continuing to set prices through marginal cost bids on a wholesale market is a road to nowhere, he believes. “What you are building is a permanent distortion. You would have to continue subsidising,” he warns. •

INTERVIEW LET MARKET FORCES RULE

Peder Østermark Andreasen, in his role as president of the European Network of Transmission System Operators for Electricity and CEO of Danish transmission system operator (TSO) Energinet.dk, has been deeply involved in integrating renewable energy into the power systems of Europe. What are his views on perhaps an even tougher challenge, integrating variable renewables without fuel costs into electricity markets that were never designed for that purpose? Andreasen talks about the ability of markets to efficiently provide the right solution and draws parallels with how the telecoms industry transformed itself.

Q: How much of a challenge is represented by the growing deployment of renewable energy with low marginal cost but a high capital cost? A: The current market model we have is certainly an important tool for integrating renewables. Without the proper price signals, we can’t integrate renewables. There is a challenge from the zero marginal cost phenomenon we see in wind and solar, and to a certain extent hydro. The amount of renewables we see entering in our region is bringing down prices. This is a challenge but also an opportunity. We see volatility and price spikes but also the opportunity to offer flexibility to stay in the market, to hedge the market. It is true that some of the conventional power plants have suffered but we see an opportunity to bring prices up.

Q: How do you see prices coming up? A: In the next decade or two it is expected that a major part of the existing generation capacity will be decommissioned. In market situations with no supply from PV or wind, prices are expected to peak, especially until demand side response in the market becomes more developed. Few hours with high prices will thus probably be a major part of the business case for conventional power plants in the future.

Q: Would volatility and price spikes also be part of the business case for renewable generators? A: This is more difficult. I think what TSOs should do is to offer access to bigger markets, allowing export to areas where the willingness to pay is higher, so linking low cost areas like the Nordics to high price areas.

Q: My understanding, however, is that weather patterns are similar across northern Europe. How could this work in practice? A: From a traditional regional point of view it’s true that the correlation of renewable energy production is pretty strong across markets. But taking the development of the Viking Link between Denmark and England as an example it is possible to extend market integration to areas where renewable energy produces in different patterns. There are potential gains by integrating markets in a true regional way and not only between neighbouring countries.

Q: Some people call for ways to stabilise the revenue of renewable generators. What do you think about that? A: We believe markets need to take care of it. We have seen other low marginal cost businesses adapt their business model. I think it will happen in this industry as well.

For example, digitalisation in the telecoms industry has meant that the industry in fact faced zero marginal costs. In this industry we have seen a shift in business models from minutes and bytes to more content based packages with integration of, for example, news services and streaming. Likewise it can be that the traditional kilowatt hour product in the electricity end user market will face competition from new offerings including energy services, mobility and potentially home automation. It’s important to say that these products don’t substitute the need for energy production and infrastructure, but business models and market places will develop to cater for a less commodity and more service oriented product definition. The new business models will probably aim at creating new value for consumers instead of “just” providing cheap electricity to appliances.

INSTEAD OF MARGINAL COST THE RESET BUTTON OPTION

To reduce investment risk, alternatives to the marginal cost approach are available that retain the use of price signals for generation dispatch

A number of specialists in electricity market design advocate scrapping the existing wholesale model based on marginal cost prices and replacing it with one that penalises neither renewable energy nor conventional generation.

Among them is Malcolm Keay at the Oxford Institute for Energy Studies. He proposes two markets for generators: an “as available” market for the variable supply from renewables; and an “on demand” market for flexible generation that can be dispatched as required. Consumers would benefit from significantly lower prices in the “as available” market, but its generators would receive support, at least initially.

The price differential between the two markets would be sufficient to provide an incentive for consumers to invest in technology such as storage or microchips in appliances that react to the presence of “as available” supply and are designed to make best use of it. Consumers would only pay the higher price for “on demand” supply if “as available” power had run short, with the option to turn off certain equipment if prices went over an agreed threshold.

Much can be done through price signals to shave peaks in demand that are expensive to cover, or encourage users to shift their demand to periods of excess generation, says Keay. Previous blunter applications of time-of-use pricing, such as reflecting over-supply through low consumer prices in the UK to encourage charging of night-storage radiators in the 1970s, led to a major shift in demand patterns, he points out.

AUCTIONS AND PPAs

Another approach as an alternative to wholesale markets, or a complementary mechanism, is providing revenues to producers through long term Power Purchase Agreements (PPAs) between buyers and sellers, a well tried and much used bi-lateral contract approach. These can be initiated by a request for generators to offer competing bids for the cost of energy from a specific volume of capacity, or awarded after an auction process.

Auctions can also be for government price support that makes up the difference between the price set by bidding and the market price paid to generators, known as Contracts for Difference in the UK. It is a model which uses price signals to dispatch the cheapest generation first, but places a safety net under renewable energy finances. Germany has moved towards a version of this model and the auction of concessions is also used to shape the Dutch and Danish offshore wind markets.

From the perspective of a renewable energy producer, auctions and PPAs have many advantages, says Francesco Venturini, global head of renewables for Italian utility Enel, a major owner of renewable energy capacity on both sides of the Atlantic Ocean. In markets like those of Europe, with prices held down by an excess of generating capacity and barriers to market exit for fossil fuel and nuclear, PPAs provide revenue certainty for investments in new renewables, says Venturini. They have worked for offshore wind, stimulating development, providing security for investors and driving down cost.

Enel is building around 1 GW of solar capacity in Mexico, costing about $1 billion and with the output contracted under PPAs. “Can you imagine us investing all that money and not having any idea of how the market will be structured, being completely exposed to market risk and not knowing if anyone will buy the power?” Venturini asks.

COPY CHILE

He points to Chile as a market that works for renewables, keeping prices low for consumers while providing investment certainty for generators like Enel. The country’s National Energy Commission oversees auctions for 20 year PPAs that are open to any technology. The contracts go to the lowest bidders who sell their generation to electricity distributors for resale to regulated customers. Wind and solar bid so low they won about 50% of the capacity on offer in an August 2016 tender.

In principle, the buyer behind the PPA can be a large pool of electricity retailers or a single large company, says Venturini. It is a market model operating in parts of Latin America, where Enel has a strong presence in renewables and also sells directly to big corporations. “In Mexico and Chile we have industrial customers while in several other countries we are also in contact with mining companies,” he says.

WindEurope sees such corporate PPAs, popular also in the US, as an emerging and “extremely relevant” trend in Europe, says chief policy officer Pierre Tardieu. But they are insufficient on their own to deliver the investment volumes needed for the EU to meet its 2030 target to trace 27% of gross energy consumption to renewable energy. About 2 GW of such deals, roughly the size of two large coal or nuclear stations, have been signed for renewables power in Europe, the majority wind.

Venturini is somewhat frustrated by the European Commission’s policy proposals for improving the design of electricity markets in its Clean Energy for All Europeans report released in November 2016, more commonly known as the Winter Package. It has some good ideas, he acknowledges, but clings firmly to the wholesale market model. “They are looking at this stuff backwards. I still think they are convinced the short-term market model could work even though they are also starting to realise that you need something parallel, with long term price signals that give investors confidence to invest in infrastructure and allow them to see a decent market return,” he says. •

BEST PRACTICE THE MARKET AS SERVANT

A reformed, flexible but still marginal-cost-based market can be designed to avoid price extremes. Flexibility is the key to curing cannibalisation

Both the International Energy Agency (IEA) and the European Commission remain convinced that wholesale markets in which electricity is traded at marginal cost are the best design for solving the energy trilemma—the supply of clean, secure and affordable energy to all. That conviction in the value of market forces is shared by industry lobby groups on either side of the conventional and renewable power divide. On this issue, electric industry association Eurelectric and green energy organisation WindEurope are in agreement. Each has provisos contentious to the other, but they do not dispute the wholesale market approach.

In its Winter Package the Commission refers to an enhanced electricity market design where “short term markets are fully developed” and “renewable generators can earn a higher fraction of their revenues from the energy markets.”

The IEA speaks in similar tones. “The transition to low-carbon power can be carried out through upgrades to existing market arrangements and regulatory instruments. The necessary upgrades can be identified in the best practices of existing electricity markets in Europe, in the Australian National Electricity Market, and in North America,” states the IEA in Repowering Markets.

The extremely dynamic electricity markets of the US, those that adopted the “standard market design” approach proposed by the Federal Energy Regulatory Commission, are arguably the best demonstrations yet that marginal cost wholesale markets can make good servants when prevented from becoming bad masters.

The undisputed advantage of a wholesale market based on marginal cost is that when it functions as intended the cheapest product is prioritised at all times. In the current electricity market, that product is renewable energy. Of the three challenges that make up the global energy trilemma, the wholesale market responds to two of them. Missing from the clean, reliable and affordable trio are investment signals to secure a reliable supply long term. To the large but cautious investor, essential for power capacity development, the prospect of ever longer periods of ever lower prices, interspersed with volatile price spikes that energy regulators may decide to cap, is not an attractive proposition.

**Creation of price signals that change patterns of customer consumption is a key task for wholesale markets**

FLEXIBILITY IS THE CURE

The solution emerging is to stop occurrences of long periods of low or negative prices caused by false scarcity signals. With tweaks to the design of wholesale markets, energy products that increase the flexibility of the power system can be attracted into them. The effect would be to stop the extreme scarcity signals that send prices through the floor and to provide new revenue streams for renewable energy producers.

Flexibility products include: voluntary reductions in demand on request, known as demand side management; adapting consumption to be more energy efficient; energy storage options like power to heat; and more cross border grid connections. The more flexible the system, the flatter the demand curve and the less likelihood of extreme surges in prices.

Putting a price on the benefits of shaving off peaks in demand that cause high prices or limiting the frequency and depth of low prices, could provide the investment signals needed. “If an actor was paid for not producing or not consuming it would be of economic value and there would be more economic income in this flexibility. And there would be new business models of how to exploit these low cost price situations,” says Peter Karnøe, professor at Denmark’s Aalborg University.

“We certainly need a way to bring in more flexibility on the demand side and that has got to be valued in some way. And quite how that happens or the dimensions of how that happens is unclear,” says Exeter University’s Mitchell.

ACTIVE CONSUMERS

For Michael Hogan of the non-profit Regulatory Assistance Project, a global organisation with American roots, the way forward is clear: creation of price signals that change patterns of customer consumption is a key task for wholesale markets.

Without demand response, he sees price volatility in current markets increasing as the share of renewables grows. The extreme scenarios of prices at zero or below for significant periods of time when these generation sources are price setters, or at sky-high levels when they are not, comes about because the market, “totally ignores demand response,” he says. “The historical assumption of inelasticity of demand is increasingly not true,” he adds. “The practical ability of consumers to act is increasingly available at increasingly affordable prices. What is missing is the rate structures and the regulatory system.”

Entering contentious waters, Graham Weale, a professor at Rhur University Bochum in Germany, believes customers can be activated by price signals. “There is a major disconnect between the prices most consumers pay and the wholesale market,” he says. If electricity bills were more closely aligned with wholesale market prices customers would be more inclined to take advantage of technology like smart meters to respond in real time to changes in prices. To reduce their exposure to peak demand prices, they could buy more efficient appliances, or agree to have non-critical devices temporarily switched off.

Some power system operators in the US already make extensive and large scale use of demand response. The Energy Reliability Council of Texas (ERCOT) has for a number of years got 50% of its supplemental reserves from demand response while a third of the new market for provision of electricity capacity in the Pennsylvania-New Jersey-Maryland system is demand response, says Hogan.

In Germany, 55% of all electricity bill recipients have never switched to a new supplier despite the opportunity to make considerable savings. Source: Bitkom poll

EXTRA REVENUES

Adding flexibility provides renewable energy generators with more options for revenue through sales of grid support services. Traditionally, such services were exclusively offered by generators able to readily dispatch bursts of power on request by burning more fuel. Paying for such services outside the market and deliberately excluding renewables from participating, has to change, says Hogan.

If the cost of procuring reserves is also accounted for by system operators, prices should not go to zero for any significant amount of time, he says. “The demand curve that is usually drawn completely ignores the demand for reserves,” he adds. Since demand for operating reserves tends to increase when renewable generation is high, Hogan says accounting for them in the demand curve should support prices. When renewables are providing 100% of energy, he notes that the system operator is sure to be running more expensive generation in the background to provide reserves, but this has often not been conveyed in wholesale prices.

ERCOT is among the system operators that have implemented what are known as operating reserve demand curves, administrative mechanisms that set the value of an incremental unit of reserves that rises gradually to the full value of lost load or to a very high price cap as the supply of reserves falls below requirements. This co-optimisation mechanism is subsequently used to create a price adder that is included in the clearing price for energy, closing the gap between the energy market price set through trading and a fuller price that includes the value of security of supply.

Hogan sees the energy-only market as working well but notes that renewable energy support will still be needed wherever there is overcapacity, as on the European continent. “In many cases, renewable energy continues to need support because the market doesn’t need incremental investments. So you need to push them in, and you also need to push out excess capacity,” he says. •

MARKET MASTERY RENEWABLES LEARN THE TRADE

Given a fit-for-purpose market design, renewables are proving they can meet power system reliability standards and keep energy affordable. The risk of a destabilising market revolution is receding as steady evolution points the way forward

In a power system built around renewables, it is renewable energy generators that must provide the services needed to run the grid. If not, consumers will be landed with the considerable extra cost of a dedicated alternative source of generation, says Jochen Kreusel, market innovation manager in the power grids division at ABB Power in Germany.

Ireland is among the front runners in demonstrating that a high penetration of renewable energy in a modern power system is feasible, affordable and meets reliability standards, even in a country with restricted interconnection capacity. Much effort has been put into designing the Irish market to be fit for purpose. Renewables not only provide grid and balancing services, they get paid for doing so, too.

“We see a lot of renewables owners and operators becoming more savvy and they are now competing in the balancing or services markets,” says Alexander Kulesh, energy analyst with Irish power trader and services provider Electroroute. “I see this as the way forward.”

Through its DS3 System Services programme, Irish system operator EirGrid is doubling the number of services it will buy to keep the system stable to 14 and quadrupling the budget for services to be procured to €235 million from an annual spend of €60 million. “Previously fixed service system tariffs were paid mainly to large generators to provide reserve systems,” says Kulesh. “Now EirGrid has added services ranging from super fast-acting reserves to long term ramping when the wind isn’t blowing and also opened up the programme to a lot of new providers.”

DS3 was developed following a study published in 2010 indicating what policies and services could be adopted to allow the Irish power system to handle about 75% of renewable energy penetration at one time. “As a small island nation with little interconnection capability, Ireland is seeing the challenges in operating a system with a large amount of renewables years before others,” notes Kulesh.

In most cases, predicting the likely revenues renewables could earn is difficult, says Kreusel. “If you had asked people a decade ago about the implications of reaching 2020 targets for renewables, you would have heard that balancing costs would be really high,” says Kreusel. “But balancing costs are at an all time low in Germany and this is not because there is no volatility. There is a lot of volatility but balancing markets have been streamlined, control areas and system operators are coordinating better and market closure times have been shortened. So the market looks a lot different than it did a decade ago.”

PAY AS BID

Peter Karnøe, professor at Aalborg University, points to a wholesale market refinement being considered. Instead of bids based on marginal cost, in some situations a better result may be achieved by pay-as-bid, in which successful bidders are paid the price offered, as used in intraday trading on Nord Pool, the Nordic power market. In theory pay-as-bid would allow for more strategic bids that also cover part of the capital cost expenditure. But for market players it is also riskier. Generators that bid too high would not sell any power while others risk getting less than they would receive under the marginal cost model, where the highest accepted bid sets the price for all.

WindEurope believes the risks are too great and marginal prices are the better market instrument. “Pay-as-bid pricing can lead to inefficiencies, among other things because small players do not have the capability to forecast prices,” it states in its Market4RES report. But it concedes the potential for a hybrid solution within an energy only market, with a marginal cost clearing price set in the day-ahead market deciding the power mix, followed by fine tuning of supply and demand in an intraday market with pay-as-bid pricing, referred to as the continuous market. “The hybrid approach can be expected to be the best design variant,” states the report.

EVOLUTION NOT REVOLUTION

Reaching agreement on what incremental changes to introduce to the design of wholesale markets and how best to implement them will not be achieved overnight. Continued support for renewables until markets are fit for purpose is advocated by WindEurope, the International Energy Agency (IEA), and other government advisory bodies.

“Reaching decarbonisation objectives by 2030 implies deploying low carbon technologies faster than existing generation is expected to retire and this situation will continue to depress prices during the energy transition,” says the IEA. The agency cautions against rapid change and expects the energy transition to be a gradual process as the interaction between technologies and market rules is steadily refined.

Evolution may indeed win the day. Windy weather in Denmark over the 2016 Christmas period, when industrial demand for electricity is low, had wind turbine owners fearing days of negative prices, heralding a financially disastrous end to the year, similar to that experienced in a previous winter holiday season. But market signals successfully triggered planned flexibility measures, underpinning prices over 29 critical hours.

Instead of the acute financial pain of a deep plunge into negative territory over days, wind turbine owners suffered no more than a relatively short and shallow dip into the icy waters of prices below zero. A feared Christmas nightmare of big losses in windy weather became a success story for market flexibility,flexible generation and savvy power system operation. •

TEXT Heather OʼBrian & Lyn Harrison/__PHOTO Palle Peter Skov for Energinet.dk & Joe Dunckley, Shutterstock